The National Quantum Strategy turns two-and-a-half years old this spring, the second of its scheduled review windows since then-science secretary Michelle Donelan set out the £2.5bn, ten-year programme in March 2023. It remains, by some distance, the largest single quantum funding commitment in Europe. Halfway through Mission Phase 1, the Department for Science, Innovation and Technology (DSIT) and the National Quantum Computing Centre (NQCC) at Harwell can fairly point to physical infrastructure delivered, a credible flagship cohort of UK companies, and a research base that remains globally competitive. The harder question — and the one Whitehall is increasingly asked by Treasury — is whether £250m a year is now structurally too small to keep Britain inside the leading group of nations.

What has actually been deployed

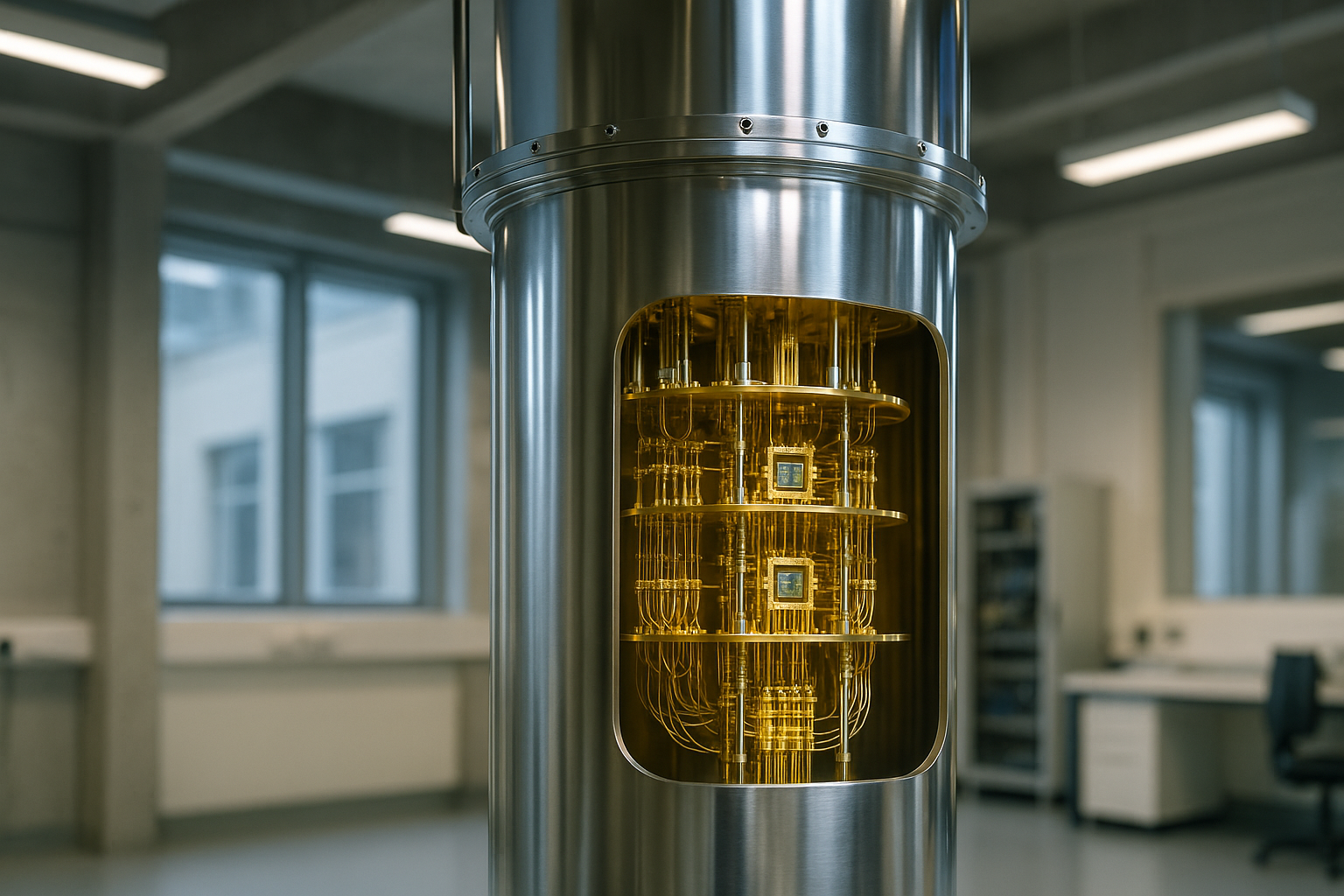

The clearest measure of progress is the National Quantum Computing Centre. The Harwell facility, opened in late 2023 at a build cost of around £93m, is now running its seven-supplier hosting challenge through to phased completion: superconducting hardware from Rigetti and Oxford Quantum Circuits, neutral-atom systems from Infleqtion and QuEra, photonic systems from ORCA Computing and Aegiq, and a trapped-ion machine from Quantinuum. By the end of FY26, the NQCC expects most cohort hardware to be installed and accessible to academic and industrial users. That represents a meaningful step-change from early 2023, when British public quantum compute was effectively run on shared time at NPL and at university hubs in Oxford, Cambridge, UCL and Sussex.

DSIT has also built out the Quantum Catalyst Fund into its second cohort, channelled over £100m of Innovate UK funding into translation projects, and signed quantum partnership memoranda with Australia, the Netherlands and South Korea. The Quantum Skills Strategy, published in 2024, has — on departmental figures — pushed doctoral places in quantum-relevant disciplines from roughly 200 a year towards 350.

Where the gap is widening

Set against this is the capital gap. PsiQuantum, founded by UK-trained physicists but now headquartered in California, has raised more in 2024 alone than the UK’s entire annual quantum strategy spend, with the Australian and Queensland governments separately underwriting a multi-hundred-million-dollar Brisbane facility. Quantinuum, headquartered in Cambridge, raised roughly $300m at a $5bn valuation in early 2024 and has signalled a US listing — not London — when the IPO market opens. Riverlane, the most strategically significant UK error-correction company, has so far funded the full sprint to its Deltaflow control system on well below $100m of cumulative capital; at US peer pace, it would have raised three to four times that.

The structural issue is not that British capital is absent. It is that pension and insurance allocators — Legal & General, M&G, Phoenix, the Universities Superannuation Scheme — still treat single-name quantum exposure as venture risk rather than infrastructure-adjacent science investment, and therefore size positions at venture weights. The Mansion House Compact and the British Business Bank’s Long-term Investment for Technology and Science (LIFTS) vehicles were intended to bridge that gap. The real-world flow into UK quantum specifically has been measured but small.

The next 18 months

Three milestones now matter. First, the NQCC’s full hosting review, which will publish performance data on each of the seven supplier systems and will be the first credible public benchmark Britain has produced. Second, the FY27 spending review, where DSIT will need to defend its quantum line against a Treasury increasingly focused on AI compute and defence. Third, the next funding rounds for Quantinuum, Riverlane and Oxford Quantum Circuits — all signalled for 2026 — which will reveal whether City money can be marshalled at scale or whether the centre of gravity quietly relocates to Massachusetts and California.

Britain has built the infrastructure phase of the quantum strategy on time and broadly on budget. The investment phase is what comes next, and it is materially harder.

Sources: UK National Quantum Strategy (DSIT, March 2023); NQCC published progress notes; Quantum Skills Strategy (DSIT, 2024); UKRI and Innovate UK Quantum Catalyst Fund; Financial Times and Sifted reporting on UK and US quantum funding rounds.

Discussion

Sign in to join the discussion.

No comments yet. Be the first to share your thoughts.